Bundling commercial vehicle insurance with broader business coverage means combining commercial auto policies with other business policies into a single coordinated package, and this approach often delivers measurable cost savings and operational simplicity. In this article, you will learn what bundling is, how multi-policy discounts and coverage layering work, and when bundling produces the biggest financial and risk-management advantages for small and mid-sized fleets.

Many business owners wrestle with separate renewal dates, duplicated coverages, and fragmented claims handling; bundling provides a coordinated solution that reduces administrative overhead and closes common protection gaps. We will cover financial benefits and modeled comparisons, explain administrative efficiencies and claims coordination, detail enhanced coverage and umbrella layering, and describe why an independent insurance agency can improve bundling outcomes.

What Are the Financial Benefits of Bundling Commercial Auto and Business Insurance?

Bundling reduces overall cost through multi-policy discounts, lower administrative expenses, and reduced duplicate coverage exposure, producing a clearer total cost of ownership for commercial fleets. The mechanism is simple: carriers reward combined premium volume and reduced transactional overhead, which often translates into percentage discounts and fewer separate fees. The specific financial benefits include premium savings, lower incidental administrative costs, and potential leverage when adding a Commercial Umbrella above primary limits.

Bundled financial benefits include:

-

Multi-policy Discounts: Combining auto and BOP often yields a direct premium reduction from carriers.

-

Lower Administrative Costs: Consolidated billing and renewals reduce bookkeeping time and accounting fees.

-

Reduced Duplicate Coverage: Unified limits and endorsements avoid overlapping payments and save money long-term.

These savings are most significant when businesses have multiple vehicles or substantial property/liability exposure, and the next subsection explains how multi-policy discounts typically work in practice.

How Do Multi-Policy Discounts Reduce Your Insurance Premiums?

A multi-policy discount is a carrier-level reduction applied when two or more qualifying policies are written together, lowering aggregate premiums through rate credits and negotiated terms. The reason this works is that combined policies increase customer retention and lower acquisition costs for insurers, which they return to policyholders as discounts or improved terms. For fleets and businesses that qualify, bundling commercial auto with a Business Owners Policy (BOP) commonly produces the clearest discount mechanics and easier premium reconciliation.

To illustrate, businesses with multiple units or vehicles often see larger discounts because premium volume improves bargaining leverage, and savings compound when secondary coverages like umbrella limits are included. Understanding eligibility and exact discount levels requires carrier quotes, which helps explain why comparing bundled offers is essential before deciding. The next subsection compares bundled versus separate policy cost drivers.

Can Bundling Commercial Insurance Save Your Business Money?

Bundling often saves money when it reduces duplicated coverages, secures multi-policy discounts, and streamlines administrative fees that accompany separate policies. The mechanism for savings includes applying a single deductible structure where appropriate, avoiding redundant endorsements, and leveraging the insurer’s willingness to price broader risk portfolios competitively. However, savings are not automatic: they depend on fleet size, claims history, and coverage chosen.

Businesses with multiple vehicles, combined property and liability needs, or frequent inter-policy claims coordination stand to gain most from bundling, while single-vehicle operations should compare quotes to confirm savings. For a precise estimate, request bundled quotes that compare the total cost of ownership (premiums + fees + expected claims impact) over 12 months, which the table below helps summarize. The following section provides a concise cost-difference comparison.

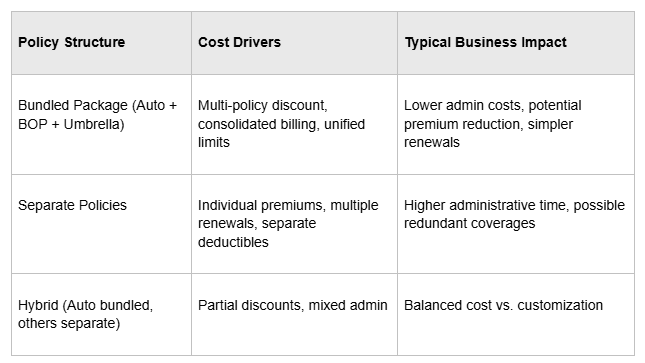

What Are the Cost Differences Between Bundled and Separate Policies?

Comparing bundled versus separate policies focuses on premium totals, deductible alignment, aggregated limits, and administration fees that affect annual cost. Bundling can lower premium totals via multi-policy discounts and eliminate duplicate fees, while separate policies may offer tailored limits per exposure but create more invoices and renewal events. The best approach is to model both scenarios to see net savings and risk trade-offs.

This comparison shows why modeled quotes matter and leads into how bundling simplifies management beyond pure dollars.

How Does Bundling Simplify Commercial Insurance Management?

Bundling simplifies management by creating a single renewal cycle, consolidated billing, and unified documentation, which reduces administrative time and improves compliance tracking. The mechanism is administrative consolidation: one file, one set of endorsements, and one agent-managed renewal reduces friction across accounting and operations teams. These operational efficiencies free time for core business tasks and reduce the chance of missed renewals or coverage lapses.

Key administrative simplifications include:

-

Single Point of Contact: One agent handles policy adjustments and claims coordination.

-

Consolidated Renewals: One renewal calendar reduces missed dates and compliance risk.

-

Unified Billing: Fewer invoices and easier reconciliation for accounting teams.

These features also affect claims handling, which the next subsection examines with practical outcomes.

What Is Streamlined Policy Administration in Bundled Insurance?

Streamlined administration means unified policy documents, one renewal negotiation, and a single compliance checklist that replaces multiple policy management tasks. This works because an agent or carrier manages endorsements and adjustments across all bundled components, reducing duplicated paperwork and audit burden. Businesses save time on renewals and can allocate resources to operations instead of insurance admin.

Adopting a bundled approach also simplifies record-keeping for regulatory compliance and internal audits, which benefits multi-state operations and fuels better strategic decision-making about limits and deductibles. The next subsection explains how bundling improves claims processing.

How Does Bundling Improve the Claims Process for Businesses?

Bundling improves claims coordination by enabling a single advocate—often the broker or agent—to manage communications across carriers and policies, reducing delays and administrative back-and-forth. The mechanism is centralized advocacy: the agent collects incident details once and coordinates which coverage triggers apply, avoiding contradictory carrier interactions. This coordination typically shortens resolution time and clarifies recovery paths for vehicle and business losses.

A consolidated claims approach also reduces the administrative burden on operations staff during stressful incidents, and it increases the likelihood that overlapping coverages, such as a Commercial Umbrella and auto liability, will be applied correctly. The following subsection highlights why a single point of contact matters.

Why Is Having a Single Point of Contact Beneficial for Business Owners?

A single point of contact centralizes expertise, speeds decision-making, and provides tailored advice during renewals and claims, which makes insurance management less disruptive to daily operations. This works because the contact maintains institutional knowledge about your portfolio, negotiates on renewal, and advises on endorsements and limits aligned with business risk. The result is faster issue resolution and more consistent policy alignment.

Businesses that operate in multiple locations or manage fleet logistics particularly benefit from having one advisor who understands both vehicle risk and broader business exposures, setting the stage for more effective coverage enhancement discussed next.

What Enhanced Coverage Does Bundling Commercial Vehicle and Business Insurance Provide?

Bundling enhances coverage by layering protections—such as coordinated liability limits and umbrella excess coverage—that close gaps between policies and increase the total available indemnity during major losses. The mechanism is complementary layering: primary policies handle first-dollar coverage, while a Commercial Umbrella supplies excess limits when primary policy limits are exhausted. This combined architecture reduces the chance of uncovered losses that would otherwise reach the business balance sheet.

Common coverage enhancements include expanded liability coordination, unified endorsements across auto and property, and streamlined umbrella integration, which the list below outlines. The following subsection describes vehicle-specific protections.

How Does Bundling Strengthen Protection for Commercial Vehicles?

Bundling strengthens vehicle protection by aligning liability and physical damage endorsements so that coverage triggers and deductibles coordinate across policies, reducing out-of-pocket exposure after complex incidents. The reason this matters is that many commercial claims involve multiple exposures—vehicle damage plus third-party liability or business interruption—which bundled policies can treat holistically. As a result, businesses often avoid coverage disputes that arise when separate carriers interpret incidents independently.

A practical example is when an accident causes vehicle damage and a business interruption claim; bundled documentation and a single claims advocate make resolution faster and more complete, which reduces operational downtime. The next subsection lists common add-on coverages.

What Additional Business Coverages Are Included in Bundles?

Bundled packages commonly include or integrate these additional business coverages to address non-vehicle exposures and extend protection across operations.

-

Commercial Umbrella: Adds excess liability limits above primary policies.

-

Commercial Property Insurance: Protects physical assets and inventory.

-

General Liability: Covers third-party bodily injury and property damage.

-

Business Owners Policy (BOP): Combines property, liability, and business interruption.

Each add-on addresses specific risks—umbrella for catastrophic liability, property for asset protection, and BOP for combined baseline coverage—and bundling ensures these parts work together to reduce coverage gaps. The next subsection explains gap-closing mechanisms.

How Does Bundling Help Close Coverage Gaps and Manage Risks?

Bundling helps close coverage gaps by performing a coordinated gap analysis and designing unified limits and endorsements that prevent coverage overlaps and holes. The mechanism is integrated policy design: an agent assesses exposures across vehicles and business operations and selects coverages that complement one another instead of duplicating benefits. This lowers uninsured risks and streamlines future audits.

Regular policy reviews after bundling ensure evolving exposures—such as fleet growth or new operational sites—are reflected in limits and endorsements, which supports long-term risk management and prepares businesses for scalable growth.

This table clarifies how administrative features translate into day-to-day business benefits and leads to why independent agencies are often the best partners for bundling.

Why Choose an Independent Insurance Agency for Bundling Commercial Insurance?

An independent insurance agency provides multi-carrier access and personalized advice, which improves the chances of securing competitive bundles and tailored terms for commercial vehicle insurance and related business coverages. The mechanism is brokered market access: independent agents compare multiple carriers and match coverage options to specific business risks, rather than offering a single carrier’s product. This broader sourcing increases competitive pressure and potential savings.

Independent agencies also serve as ongoing advisors during claims and renewals, which is especially useful for businesses operating across jurisdictions. The next subsection describes a specific agency’s approach.

How Does Brook Insurance Associates LLC Offer Competitive Bundling Solutions?

Brook Insurance Associates LLC is an independent insurance agency based in Warwick, RI that serves clients in RI, CT, MA, VT, NV, and FL and emphasizes competitive rates from multiple carriers, personalized service, and expert advice. Their approach to bundling focuses on sourcing competitive offers across carriers and structuring packages—such as Business Auto Insurance and Business Owners Insurance—so clients can evaluate bundled quotes effectively. Using the agency’s experience helps business owners compare bundled versus separate scenarios without the administrative burden of soliciting multiple insurers.

Brook Insurance Associates LLC

Brook Insurance Associates LLC is located at 1935 Elmwood Ave, Warwick, RI 02888. They offer a variety of personal and business insurance solutions, including auto, home, and commercial insurance. The agency is licensed in multiple states, including Rhode Island, Connecticut, Massachusetts, Vermont, Nevada, and Florida.

Clients have praised Brook Insurance Associates LLC for their personalized service and competitive rates. For example, one client mentioned that they have been using Chris Brook since the inception of their business in 2006 and wouldn’t go anywhere else.

By partnering with an independent agency like Brook Insurance Associates LLC, business owners can benefit from tailored bundling solutions that align with their specific needs and operational requirements.

How Does Licensing in Multiple States Benefit Your Business Insurance Needs?

Licensing in multiple states ensures compliance and market access for businesses that operate across state lines and require consistent coverage in each jurisdiction where vehicles or operations are located. Brook Insurance Associates LLC is licensed in the states provided, enabling them to source appropriate carrier options and ensure regulatory compliance for multi-state fleets. The practical benefit is simpler account management and consistent policy structures across jurisdictions.

This multi-state capability reduces the administrative complexity of managing separate local agents and supports cohesive coverage for expanding businesses.

What Do Local Businesses Say About Bundling Commercial Insurance in Rhode Island?

Local businesses often report measurable administrative improvements and clearer cost visibility after bundling commercial insurance, noting fewer invoices and a single renewal calendar as primary operational wins. Anonymized summaries indicate that the main mechanisms behind positive outcomes are multi-policy discounts and centralized claims advocacy, which reduce downtime and accounting burden. These local experiences highlight why many Rhode Island businesses consider consolidation when managing commercial vehicle fleets and broader business risks.

The next subsection provides a modeled scenario of savings and encourages steps to obtain a personalized estimate.

How Have Rhode Island Businesses Saved Money by Bundling?

Rhode Island businesses typically realize savings through combined discounts and reduced duplicate coverage, especially when they have multiple vehicles and significant property or liability exposures. The mechanism is consolidated pricing and elimination of overlapping endorsements, which reduces the effective premium burden and administrative fees. Modeled scenarios that compare bundled quotes against separate policies show improved total cost of ownership for many multi-vehicle operators.

Businesses are encouraged to request bundled quotes to see exact savings based on their fleet size, claims history, and chosen limits.

What Operational Improvements Have Local Businesses Experienced?

Operationally, local firms report streamlined renewals, faster claims handling due to single-agent advocacy, and simplified accounting from consolidated billing, which together reduce internal administrative hours. The mechanism behind these improvements is centralization: fewer vendor relationships and one renewal negotiation replace multiple simultaneous tasks. This operational clarity supports more predictable budgeting and easier regulatory compliance.

These improvements make it practical for owners to focus on growth rather than insurance administration.

Where Can You Get a Customized Commercial Insurance Bundle Quote?

To obtain a customized commercial insurance bundle quote, prepare fleet details, vehicle types, current policy documents, and recent loss history to enable meaningful comparisons between bundled and separate scenarios. Brook Insurance Associates LLC offers personalized quote assistance for Business Auto Insurance, Business Owners Insurance, and Commercial Umbrella products, and its multi-carrier approach helps businesses evaluate competitive bundled options. Providing clear operational details up front speeds the quoting process and produces more accurate estimates.

Gathering these documents and contacting an independent agent is the most effective next step to compare bundle vs. separate policy outcomes.