Commercial vehicle insurance premiums climbed nearly 10 percent, putting pressure on fleet budgets and exposing businesses to liability gaps. Business owners need a clear roadmap to select coverage that aligns with operational risks and state requirements. This guide defines commercial vehicle insurance, explores essential coverage types, cost drivers, Rhode Island mandates, and provider selection tips—empowering companies to protect vehicles, assets, and reputation.

Commercial Auto Insurance Premiums Rise in Early

Commercial auto insurance premiums saw significant increases in the first two quarters, with rates climbing between 9% and 9.8%. This trend reflects persistent underwriting losses and rising claim costs in the market, impacting policyholders across the industry.

This research directly supports the article’s opening statement regarding the increase in commercial vehicle insurance premiums.

What Is Commercial Vehicle Insurance and Why Does Your Business Need It?

Commercial vehicle insurance protects business-use cars, vans, trucks, and fleets by combining liability, physical damage, and optional endorsements into a single policy structure. Underwriters assign coverage modules with specific limits and deductibles, ensuring companies safeguard assets, minimize legal exposure, and maintain regulatory compliance.

What Does Commercial Vehicle Insurance Cover?

Primary commercial vehicle insurance packages include multiple coverages to address third-party liabilities and vehicle losses:

-

Bodily Injury Liability: Pays medical and legal costs when an insured driver injures others.

-

Property Damage Liability: Covers repair or replacement of third-party property damaged by a business vehicle.

-

Collision Coverage: Funds repairs for impact damage regardless of fault.

-

Comprehensive Coverage: Insures against non-collision events such as theft, vandalism, and weather.

These core coverages form the foundation for tailored protection and bridge into specialized add-ons for unique business needs.

Who Needs Commercial Vehicle Insurance?

Any business that deploys vehicles for day-to-day operations requires a commercial policy to avoid coverage exclusions and legal penalties:

-

Delivery services, couriers, and logistics firms

-

Contractors, landscapers, and service providers

-

Taxi, limousine, and rideshare operators

-

Owner-operators and fleet managers

Identifying your operation’s vehicle use clarifies which policy modules best align with risk exposure.

How Is Commercial Vehicle Insurance Different from Personal Auto Insurance?

Key distinctions between commercial and personal auto policies influence coverage design:

Understanding these differences ensures businesses choose policies built for higher liability exposures and complex operational needs.

What Are the Key Coverage Types in Commercial Vehicle Insurance?

Coverage types define the range of protection in a policy by addressing liability, vehicle damage, and optional business risks. Insurers group these into primary and add-on modules, allowing companies to customize protection and control costs.

What Is Liability Coverage and Why Is It Essential?

Liability coverage compensates third-party costs when a company vehicle causes harm:

-

Bodily Injury Liability supports medical expenses and legal fees for injured parties.

-

Property Damage Liability pays to repair or replace damaged structures and vehicles.

Maintaining adequate liability limits protects the company’s assets from costly judgments.

How Do Collision and Comprehensive Coverage Protect Your Vehicles?

Physical damage modules cover different perils:

Pairing these coverages preserves fleet value and minimizes out-of-pocket repair costs.

What Additional Coverages Should Businesses Consider?

Beyond core protections, specialized modules address niche risks:

-

Uninsured/Underinsured Motorist: Compensates for damage when at-fault drivers lack adequate coverage.

-

Cargo Insurance: Protects goods in transit against loss or damage.

-

Hired and Non-Owned Auto: Extends liability to rented vehicles and employee-owned cars used for work.

-

Personal Injury Protection (PIP): Covers medical bills and lost wages for insured occupants.

Adding these ensures comprehensive risk management for complex operations.

What Factors Affect the Cost of Commercial Vehicle Insurance?

Insurance premiums reflect multiple variables, including vehicle specifics, driver profiles, and coverage choices. Underwriters weigh each risk factor to set rates, so understanding cost drivers helps businesses optimize budgets.

How Do Vehicle Type and Usage Impact Your Premium?

Vehicle characteristics and deployment patterns strongly influence rates:

-

Heavy-duty trucks generally incur higher premiums than light vans.

-

Dedicated delivery routes may pose a lower risk compared to unpredictable long-haul assignments.

-

Larger fleets benefit from volume discounts but face aggregate exposure.

Choosing appropriate vehicle categories and usage patterns can reduce insurance costs.

How Does Driver History and Safety Affect Insurance Rates?

Driver performance and safety programs shape underwriting decisions:

-

Clean driving records signal lower accident risk.

-

Ongoing safety training and telematics monitoring demonstrate risk management commitment.

-

Frequent violations or claims history can trigger rate surcharges.

Implementing robust safety initiatives improves underwriting outcomes.

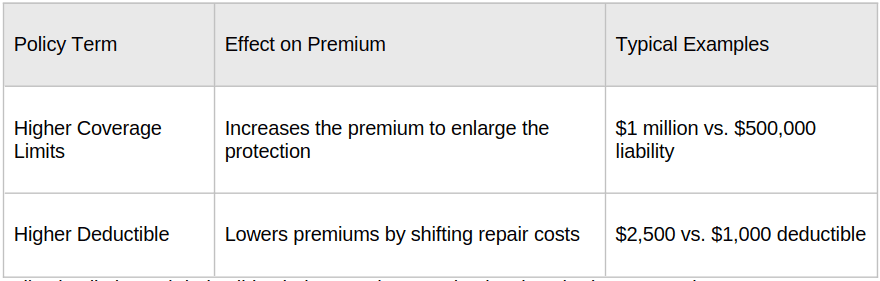

What Role Do Coverage Limits and Deductibles Play in Cost?

Policy structures balance premium affordability against financial exposure:

Adjusting limits and deductibles helps match protection levels to budget constraints.

What Are the Commercial Vehicle Insurance Requirements in Rhode Island?

Rhode Island mandates state minimum liability limits for business vehicles to operate legally. The DMV enforces proof of coverage at registration and renewal, so meeting these requirements avoids citations and vehicle suspensions.

What Are Rhode Island’s Minimum Liability Coverage Limits?

Rhode Island law requires these base limits:

-

$25,000 bodily injury per person

-

$50,000 bodily injury per accident

-

$25,000 property damage per accident

Rhode Island Commercial Auto Insurance Minimum Liability Requirements

Rhode Island state law mandates specific minimum liability limits for commercial auto policies: $25,000 for bodily injury per person, $50,000 for bodily injury per accident, and $25,000 for property damage per accident. Higher limits may be required for certain vehicle types, such as those used for transporting people for a fee.

This information verifies the specific minimum liability coverage limits and industry-specific mandates for commercial vehicles operating in Rhode Island, as detailed in the article.

Are There Industry-Specific Insurance Mandates in Rhode Island?

Certain sectors face additional coverage obligations:

-

Taxi and limousine services often require higher liability and collision limits.

-

Non-emergency medical transport (NEMT) must carry specific passenger liability endorsements.

-

Hazardous material carriers need dedicated endorsements for cargo risks.

Verifying industry-specific mandates avoids fines and operational interruptions.

How Do Rhode Island DMV Regulations Affect Your Policy?

The Rhode Island Division of Motor Vehicles enforces:

-

Proof of insurance at vehicle registration and renewal

-

SR-22 filings for high-risk drivers or lapses in coverage

-

Endorsement requirements for specialized vehicle classes

Staying current with DMV rules prevents administrative penalties and protects fleet continuity.

How Can You Choose the Best Commercial Vehicle Insurance Provider?

Selecting an insurer involves evaluating financial strength, service quality, and product alignment. A systematic comparison ensures reliable coverage, responsive support, and competitive pricing.

What Should You Look for in an Insurance Company?

Key evaluation criteria include:

-

Financial Stability: Strong ratings indicate the ability to pay claims promptly.

-

Local Expertise: Familiarity with Rhode Island regulations and business conditions.

-

Policy Customization: Flexibility to tailor coverage modules to unique fleet needs.

-

Claims Network: Access to preferred repair facilities and efficient adjusters.

These factors build trust and reduce downtime after incidents.

How Does the Claims Process and Customer Service Affect Your Experience?

A streamlined claims workflow and dedicated support team minimize disruption:

-

Digital claim submissions and status tracking speed up settlements.

-

Dedicated adjusters provide personalized guidance during recoveries.

-

Responsive customer service resolves questions and policy changes efficiently.

Strong service capabilities enhance overall risk management and satisfaction.

How Can You Compare Quotes and Find Discounts?

Smart shopping and risk-management practices unlock savings:

-

Multi-vehicle Discounts aggregate fleet business for lower rates.

-

Safety Program Credits reward documented training and telematics integration.

-

Bundling Policies (e.g., general liability with auto) often yields premium reductions.

-

Loss-Free Track Records earn loyalty credits over time.

Comparing offers side-by-side ensures the best balance of coverage and cost.

Commercial vehicle insurance is a critical safeguard for any company that relies on cars, vans, or trucks. By understanding core coverages, Rhode Island requirements, cost influences, and provider criteria, business owners can secure policies that protect assets, comply with regulations, and support long-term growth. Local agencies bring specialized expertise in state laws and customized solutions, making the selection process both strategic and seamless. Start the conversation with a trusted advisor today to get a tailored commercial vehicle insurance quote and drive your operations forward with confidence.